Opening a bank account is a key step in managing your money, building a financial history, and reaching your life goals. Whether you’re new to banking, moving to a new country, or simply looking for better features, understanding the process can save you time and stress.

Many people feel confused by the paperwork, requirements, and options available. The truth is, opening a bank account is much easier when you know what to expect. This guide will walk you through every step, from choosing the right account to making your first deposit, so you can start banking with confidence.

Why You Need A Bank Account

A bank account is not just a place to keep your money safe. It’s your entry point to modern financial services. With a bank account, you can:

- Receive your salary directly from your employer

- Pay bills easily, online or in-person

- Save money for emergencies or future plans

- Build credit history for loans or credit cards

- Shop online and make digital payments

- Access ATM withdrawals and transfers anytime

Without a bank account, you may pay extra fees to cash checks, have trouble renting an apartment, or find it hard to get a loan. In many countries, employers and landlords require you to have a bank account.

Types Of Bank Accounts

Banks offer several types of accounts, each with different features and purposes. Understanding these options helps you pick the account that fits your needs.

Checking Account

A checking account is designed for everyday transactions. You can deposit money, pay bills, withdraw cash, and use a debit card. Most checking accounts offer:

- Unlimited deposits and withdrawals

- Online and mobile banking

- ATM access

- Direct deposit for paychecks

Some checking accounts charge monthly fees, but many waive these if you maintain a minimum balance or set up direct deposit.

Savings Account

A savings account helps you set money aside and earn interest. It’s a safe place for your emergency fund or long-term goals. Savings accounts usually offer:

- Interest on your balance (rates vary)

- Limited monthly withdrawals (often 6 per month)

- Lower fees if you keep a minimum balance

Interest rates are usually higher than checking accounts, but you can’t use a savings account for everyday spending.

Student Accounts

If you’re a student, many banks offer special student accounts. These usually have:

- No or low monthly fees

- Lower minimum balance requirements

- Perks like free ATM withdrawals or discounts

You may need to show proof of student status to qualify.

Business Accounts

A business account is for companies or self-employed people. It keeps your business and personal finances separate. Business accounts offer:

- Features for tracking expenses and income

- Tools for payroll and invoicing

- Access to loans or credit lines

Banks may require business registration documents to open this type of account.

Certificates Of Deposit (cds) And Money Market Accounts

For higher interest, you might consider a certificate of deposit (CD) or money market account. These accounts pay more, but you must agree to keep your money in the account for a set period (CD) or meet higher minimum balances (money market).

Choosing The Right Bank

Not all banks are the same. Picking the right bank can save you money and frustration. Here are some factors to consider:

- Location and ATM network: Is there a branch or ATM near you? Does the bank offer free ATM access nationwide?

- Fees: Watch for monthly maintenance fees, ATM fees, overdraft charges, and other costs.

- Online and mobile banking: Does the bank have a good app or website for managing your account?

- Customer service: Is help available in your language or during hours you need?

- Interest rates: For savings, compare how much interest you can earn.

- Account features: Look for special offers, rewards, or tools that match your needs.

Comparing Bank Features

Here’s a comparison of three common bank options to help you see the differences:

| Bank Type | Monthly Fee | ATM Network | Online Banking | Minimum Balance |

|---|---|---|---|---|

| Traditional Bank | $10–$15 (often waived) | Large, national network | Yes, usually strong | $100–$1,500 |

| Online Bank | Often $0 | Partner ATMs, often free | Excellent | $0–$100 |

| Credit Union | $0–$10 | Regional or shared network | Varies | $5–$100 |

Non-obvious insight: Online banks often pay higher interest on savings and have fewer fees, but you can’t visit a branch. Credit unions may offer better rates and service, but you must qualify for membership.

What You Need To Open A Bank Account

Before you visit a bank or apply online, gather the required documents. Banks must follow laws to verify your identity and prevent fraud.

Common Requirements

Most banks will ask for:

- Government-issued photo ID: Such as a passport, driver’s license, or state ID card.

- Social Security number (SSN) or Tax ID: For US residents, this is required. In other countries, a national ID or tax number may be needed.

- Proof of address: A recent utility bill, lease, or official letter showing your name and address.

- Initial deposit: Some banks require you to deposit a minimum amount (often $25–$100).

- Date of birth: You must usually be at least 18 years old (or have a parent/guardian if younger).

- Student or business documents: If opening a student or business account, bring proof like a student ID, acceptance letter, or business registration.

Tip: If you’re not a US citizen, many banks accept foreign passports and an Individual Taxpayer Identification Number (ITIN). Some banks also offer accounts for people without standard documents—ask about “second chance” or “basic” accounts.

Preparing Your Documents

Keep your documents organized in a folder. Double-check that names and addresses match on all documents. If anything is missing or expired, fix it before you apply.

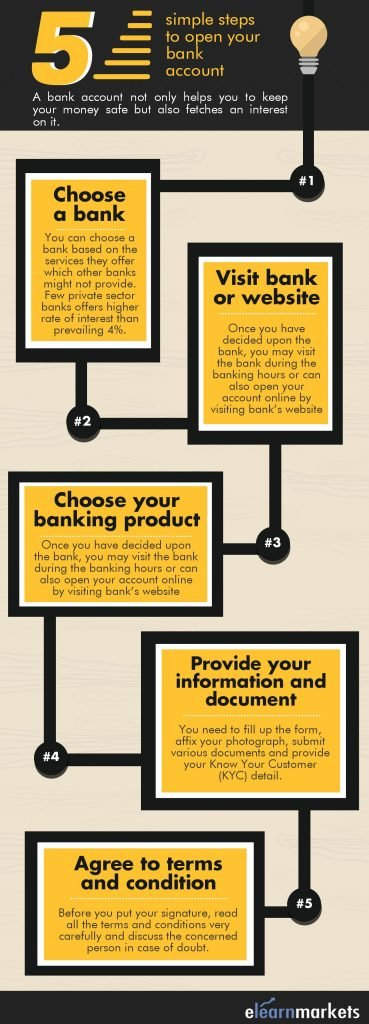

Steps To Open A Bank Account

The process to open a bank account is similar at most banks. Here’s what to expect:

1. Decide How You’ll Apply

You can open most accounts in three ways:

- In person: Visit a branch and speak with a banker.

- Online: Complete the application on the bank’s website.

- By phone: Some banks let you apply by calling customer service.

Non-obvious insight: Online and phone applications are often faster, but in-person visits can be helpful if you have questions or unusual documents.

2. Fill Out The Application

You’ll need to provide personal information:

- Full legal name

- Date of birth

- Address and phone number

- Social Security number or other ID

- Employment details (sometimes)

Be honest and accurate. False information can cause delays or denial.

3. Submit Your Documents

Upload, email, or show your documents as required. Banks may scan your ID and keep copies for their records.

4. Make Your First Deposit

Most banks require an initial deposit to activate your account. You can:

- Deposit cash

- Write a check

- Transfer from another account

- Use a debit or credit card (some online banks)

Ask about any waiting period before you can use your money—deposits by check or transfer may take a few days to clear.

5. Set Up Online Banking

Once your account is open, register for online or mobile banking. This lets you:

- Check balances

- Transfer money

- Pay bills

- Set up account alerts

Create a strong password and enable two-factor authentication for safety.

6. Receive Your Debit Card And Checks

The bank will mail you a debit card and, if requested, checks. Activate your card as instructed—often by phone or online. Sign the back of your card right away.

7. Start Using Your Account

Your account is ready! Set up direct deposit with your employer, schedule bill payments, and start managing your money.

Online Vs. In-person Account Opening

Choosing between online and in-person account opening depends on your needs and comfort level.

| Method | Speed | Document Handling | Personal Assistance |

|---|---|---|---|

| Online | Fastest (often minutes) | Upload or enter info | Limited (chat or phone) |

| In-Person | Slower (30–60 minutes) | Show originals | Direct help |

Practical tip: If you have non-standard documents, questions about account types, or need help in your language, visiting a branch is best. For simple needs and standard IDs, online is quick and convenient.

Common Mistakes To Avoid

Even though opening an account is straightforward, many people make mistakes that cause frustration. Here’s how to avoid them:

- Missing documents: Double-check all required paperwork before you apply.

- Ignoring fees: Read the fee schedule so you know about monthly charges, overdrafts, and ATM fees.

- Choosing the wrong account: Make sure the account matches your needs—savings accounts aren’t for frequent spending, and business accounts are for business use only.

- Not reading the terms: Important details about interest, limits, and features are in the fine print.

- Skipping account alerts: Set up text or email alerts to catch problems early, like low balances or suspicious activity.

- Forgetting to update information: If you move or change your phone number, let your bank know right away.

- Using weak passwords: Strong passwords and two-factor authentication help protect your money.

Non-obvious insight: If you’re new to a country, some banks offer special accounts for newcomers, with fewer requirements and extra support. Always ask if such options are available.

What Happens After You Open Your Account

Once your account is active, start building good habits:

- Monitor your transactions: Check your account regularly for mistakes or fraud.

- Keep your balance above minimums: Avoid fees by meeting the minimum balance or setting up direct deposit.

- Save receipts and statements: These help resolve disputes and track your budget.

- Understand holds: Some deposits (like checks) may take days to clear. Don’t spend money until it’s fully available.

- Link to payment apps: Connect your account to apps like PayPal, Venmo, or Apple Pay for easier payments.

Upgrading Or Closing Your Account

If your needs change, you can upgrade to another account type or close your account. Most banks require you to visit in person or call to close an account. Make sure all checks have cleared and all automatic payments are switched before you close.

Special Considerations For Non-residents And Newcomers

If you’re new to a country, opening a bank account can feel harder. But most banks have solutions for non-residents, immigrants, and international students.

What You Might Need

- Passport (foreign or domestic)

- Visa or immigration document

- Proof of address (can be a letter from your school or employer)

- ITIN or equivalent tax number (if available)

Some banks partner with universities or companies to make the process easier. Ask about international or “newcomer” accounts, which may have fewer requirements.

Real-world example: In the US, several banks accept an ITIN instead of a Social Security number. In the UK and Canada, banks may let you use a letter from your school as proof of address.

Opening An Account As A Minor

If you’re under 18, you usually need a parent or guardian to open a joint account with you. This helps you learn money skills early and build your history.

Digital Banks Vs. Traditional Banks

Today, you can choose between digital-only banks (sometimes called neobanks) and traditional banks with branches. Each has pros and cons.

| Bank Type | Pros | Cons |

|---|---|---|

| Digital Bank | No branches needed; 24/7 access; low fees; good apps | No in-person help; limited cash deposits |

| Traditional Bank | Branch support; full range of services; cash handling | More fees; may require visiting a branch |

Practical tip: If you often deal with cash or need personal help, a traditional bank may be better. If you prefer digital tools and low fees, try a digital bank.

How To Switch Banks

Sometimes your first bank isn’t the best fit. Switching banks is easier than you might think. Here’s how:

- Open your new account first. Make sure it’s active and ready.

- Move your automatic deposits and payments to the new account. Contact your employer and any companies that take payments from your account.

- Transfer your balance to the new account.

- Monitor both accounts for a month to catch any missed payments.

- Close your old account when you’re sure all payments have switched.

Non-obvious insight: Some banks offer “switch kits” or services that help move your payments for you. Ask if this is available—it can save you hours.

How Banks Keep Your Money Safe

Banks use many layers of security to protect your funds:

- FDIC or similar insurance: In the US, the FDIC insures deposits up to $250,000 per person, per bank. Other countries have similar systems.

- Encryption: Bank websites and apps use strong encryption to keep your data safe.

- Fraud monitoring: Banks watch for unusual activity and can block suspicious transactions.

- Alerts: You can set up text or email alerts for large withdrawals or low balances.

Tip: Never share your PIN or passwords. If you get a suspicious call or message, contact your bank directly.

For more about banking security, visit the FDIC’s official website.

Frequently Asked Questions

How Long Does It Take To Open A Bank Account?

It depends on the bank and method. Online accounts can be opened in minutes if you have all your documents. In-person, it may take 30–60 minutes. If your documents need extra checks, it might take a few days.

Can I Open A Bank Account With Bad Credit?

Yes. Most banks do not check your credit for basic checking or savings accounts. If you have a history of unpaid fees at other banks, you may need a “second chance” account. These have fewer features but help you rebuild your record.

What Is The Minimum Deposit To Open A Bank Account?

This varies by bank and account type. Many accounts require $25–$100 as a first deposit, but some online banks have no minimum. Always check before you apply.

Can I Open A Bank Account If I’m Not A Us Citizen?

Yes, many banks accept passports, visas, and ITINs from non-citizens. Requirements are different for each bank. Ask about special accounts for newcomers or international students.

What Should I Do If My Application Is Denied?

Ask the bank why. Often, it’s because of missing documents or issues with your banking history. You can try another bank or ask about “second chance” accounts. Fix any errors or unpaid fees before applying again.

Opening a bank account is one of the best steps you can take for your financial health. By understanding your options, preparing your documents, and making smart choices, you’ll enjoy safer money management and more opportunities. Take your time, ask questions, and choose the bank and account that fit your life.

With these steps, you’ll be set for a strong financial future.